The FleetPro Blog: The Taxman's Car Share

Getting tax relief for employees' business motoring

The Taxman's Car Share

The Taxman's Car Share

1 July 2020

You can get the taxman to pay towards your employee's car running costs for business motoring

We explain how it works and what to do.

Tax Relief For Business Motoring

If employees use their own cars on business travel they will normally be eligible for tax relief on the car's running costs.

In layman's terms that means HM Revenue & Customs will give the employee money towards every business mile they travel in their own car.

And the more business miles the employee travels each tax year, the more tax relief they get.

Also, if an employee gives up a company car and takes a cash allowance instead, the employee will normally stop paying tax on company car benefit and instead pay tax on the cash allowance, but can then offset some of the car's running costs against tax for each business mile travelled.

How Is Tax Relief Given for Business Motoring?

Tax relief is given through fixed pence per mile allowances which include a tax deduction for each business mile travelled during the tax year.

The system is called 'MAPs' (HMRCs' Mileage Allowance Payments).

What is MAPs?

Under 'MAPs' you can pay your employees a tax-free mileage-based allowance for using their car for business motoring.

The allowance is intended to cover the costs of running a car, such as depreciation, maintenance, fuel, insurance and the tax disc.

Alternatively, the employee can claim tax relief for business motoring at the MAPs rates if (s)he doesn't receive a mileage allowance or if the mileage allowance is less than the MAPs rate.

How does MAPs work?

Under the MAPs system, HMRC sets two tax-free mileage allowance rates:

- The full rate can be paid tax-free to for the first 10,000 business miles travelled in the tax year.

- The lower rate can be paid tax-free for business mileage over 10,000 miles during the tax year.

You can find details of the current MAPs rates by clicking on this link.

If you pay more than the total allowed under the MAPs scheme then the excess amount is taxed.

Why Two MAPs Rates?

HMRC considers that fixed costs such as insurance and the annual tax disc don't vary, no matter how many miles you drive each year.

As the amount of the full rate of MAPs allowance includes a proportion of these fixed costs, once the employee has travelled more than a certain number of business miles each tax year the employee will have been given tax relief in full for the fixed costs.

So, once an employee exceeds the business mileage limit, for any travel over and above the limit (s)he only needs to be given tax relief at a lower rate to cover just the variable costs (depreciation, etc) and not the fixed costs.

In other words, the employee gets tax relief above the business mileage limit only for the costs that continue to increase with each additional mile travelled (such as depreciation, maintenance and fuel).

Advisory Fuel Rates

HMRC also sets tax-free mileage allowance rates just to cover fuel costs incurred by employees on business motoring.

The mileage rates for cars with internal combustion engines (e.g. petrol and diesel) vary according to the type of fuel for the car and the size of the car's engine.

The mileage rate for electric cars is currently a single fixed rate for all types of electric car.

Click on this link to see the current rates.

The mileage rates can be paid tax-free, typically where:

- An employee has a company car and is being reimbursed for fuel costs on business travel.

- An employee already receives a cash allowance instead of a company car and is just being reimbursed for fuel costs on business travel.

What if You Pay a Cash Allowance?

If you pay a monthly or annual cash allowance, or a mixture of a cash allowance and a mileage based allowance, your employees can still claim tax relief based on the MAPs rates for the business miles travelled.

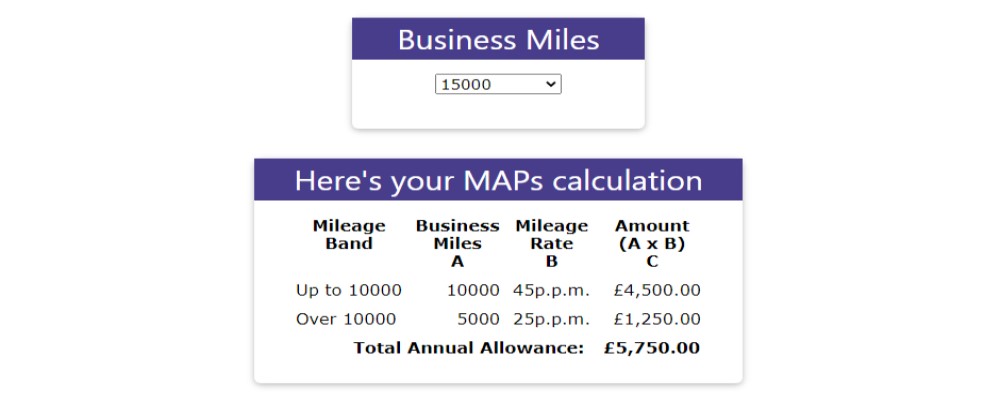

MAPs Tax Relief Example

Let's say an employee travel 20,000 business miles each tax year and receives from you;

- a fixed cash allowance of £5,000pa; plus

- 10ppm for each business mile travelled, total £2,000pa (20000 business miles @ 10ppm).

Your contribution towards the employee's business motoring costs would then be £5,000 plus £2,000, a total of £7,000pa.

Tax relief under MAPs would be:

- first 10,000 miles x 45p = £4,500, plus

- remaining 5,000 business miles at 25ppm = £1,250; a total of £5,750 tax relief.

As you pay you a total of £7,000pa and tax relief is £5,750, out of the £7,000 the employee receives from you (s)he would pay tax on £1,250 (£7,000 - £5,750).

Take a look at our sister site's tax relief calculator for live interactive examples.

What if You Don't Pay Any Allowances?

You do not have to actually pay a cash allowance or the MAPs allowances for the employee to benefit from them.

For example, if you pay only the employee's salary, or a mileage allowance that is lower than the MAPs rate, the employee can opt to claim tax relief for business use of their own car using MAPs rates.

Let's say the employee travels 20,000 business miles in their own car during the tax year and does not receive a tax-free mileage allowance from you - the employee could then claim tax relief by reference to 10,000 miles at the full MAPs rate and 10,000 miles at the lower rate.

Alternatively, if you paid a tax-free mileage allowance of only 20pence per mile for all business mileage the employee could claim tax relief on the difference between the total due under the MAPs rates and the actual mileage allowance received each tax year.

Can Employees Claim Tax Relief In Advance Under PAYE?

Employees do not need to wait until the end of the tax year to claim tax relief under the MAPs system.

They can make an advance claim at the beginning of the tax year for their Pay As You Earn ('PAYE') code number to be adjusted to take account of MAPs.

This can be useful if you pay a monthly allowance with tax deducted (and perhaps also National Insurance Contributions) under the PAYE system.To make a claim in advance for tax relief under PAYE, the employee simply provides the tax office with an estimate of business mileage for the tax year and asks for the PAYE code number to be adjusted to take account of the MAPs relief for tax year.

The employee's tax code number will then be increased by the estimated tax relief due, which will reduce the tax that the employee pays through the PAYE system, in effect, giving the employee 1/12th of their MAPs tax relief each month.

What About National Insurance Contributions?

Normally the payment of MAPs allowances within the requirements of HMRCs' rules will qualify for exclusion from National Insurance Contributions.

In strictness, for NIC purposes there is no upper threshold on mileage for paying the full rate of MAPs allowance.

This means that you could pay the MAPs rate in full without the 10,000 mile restriction for all business mileage and not have to pay NIC on the amounts received.In practice though, employer's rarely operate a separate approach to tax and NIC as far as MAPs is concerned and typically pay the same amount for both tax and NIC purposes.

MAPs Calculator

We've put together a calculator to help you and your employees compare a car's running costs to the MAPs allowance rates.

Our calculator will estimate the running costs for a new car and then compare it to the MAPs allowance rates.

We'll show whether or not the employee could be out of pocket using their own car for business mileage.

Click on this link to get started.

Related Tools

Related Posts

What Else Do We Do?

FleetPro has a unique suite of free online tools to help you find the right car.

Take a look at some of our amazing calculators and decision tools for new car buyers.

-

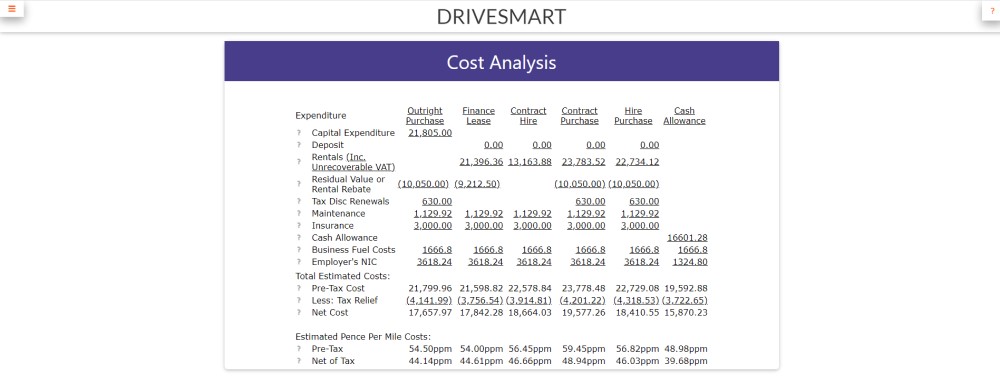

Lease or Buy?

Could you lease a new car for less than the cost of buying? Our lease calculator will work out the best finance method for you. -

ICE or Electric?

Would an electric car be cheaper than petrol or diesel? Our ICE or electric calculator compares running costs instantly. -

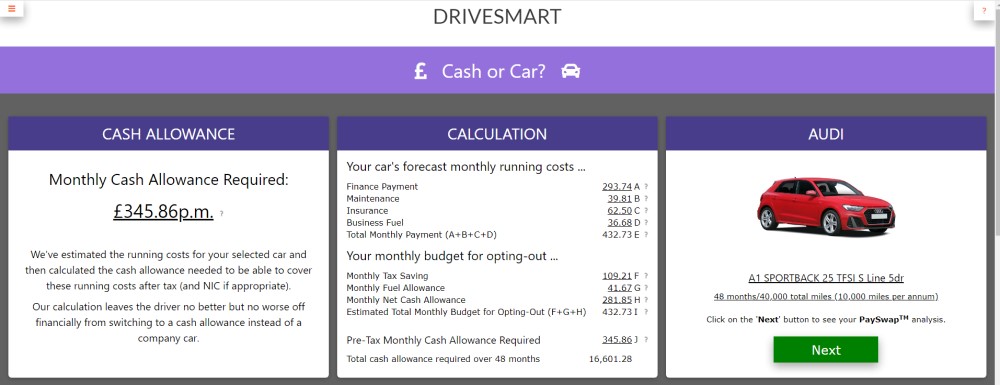

Cash or Car?

Could you give up your company car for a cash allowance? Our 'cash or car' calculator will tell you. -

Car Search

Find your next new car by monthly payment, standard equipment, performance, economy and more .... -

fleetpro.co.uk

Why not visit our fleetpro.co.uk website and see for yourself the amazing range of tools and analysis? We'll keep your place here while you browse.