The FleetPro Blog: Tax Relief For Company Car And Van Loans

We explain the complex rules ....

Tax Relief For Company Car And Van Loans

Tax Relief For Company Car And Van Loans

1 July 2020

Tax relief for interest on a loan to buy a company car or van is given according to the interest paid each year.

How Does Tax Relief On Loans Work?

The loan repayments made during the year need to be split into the repayment of the original amount borrowed and the interest charged.

This can be done on either a full actuarial basis by calculating the monthly or yearly interest, or by a simplified method known as the 'Rule of 78'.

The interest apportioned to the year is then normally tax deductible in full, subject to the tax status of the business.

Actuarial Basis

On the actuarial basis the loan interest is calculated for each year of the loan according to the repayment schedule, the amount of the original loan repaid during the year and the interest due on the outstanding balance of the loan.

Click here to see an example of how loan interest is calculated.

Rule of 78

Under the Rule of 78 the total interest charged on the loan is split to mathematically attribute the interest to each loan repayment.

To do this the total interest is divided by the sum of the months of the term.

For example, over a 36 month term the sum of the months of the term is 632, e.g. 36 + 35 + 34 + 33 etc.

The interest is then attributed backwards from the last month of the loan term, for example 1/632 in the last month, 2/632 in the 2nd from last month and so on until 36/632 in the first month.

If the interest is £1000 over the life of the loan this then would be:

£1000/632 x 36 in month 1

£1,000/632 x 35 in month 2, etc.

For example:

£1000/632 x 36 in month 1 = £56.96

£1000/632 x 35 in month 2 = £55.38

£1000/632 x 34 in month 3 = £52.22

and so on to the 12th month.

In this way the total interest attributed to the first 12 months would be £563.29, for the second year £332.28 and the third year £104.43, total £1000.

It doesn't matter whether or not the profile of the actual annual loan interest for the term of the loan matches the Rule of 78 result - the result gives an approximate amount of interest each year which is normally acceptable for accounting and tax purposes.

Self-employed

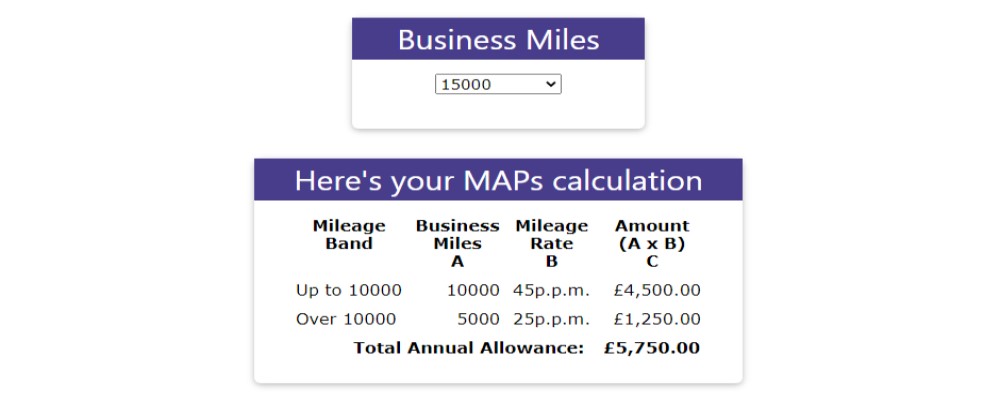

For the self-employed where the vehicle is used partly for non-business purposes, tax relief is apportioned according to the ratio of annual business miles to total annual miles.

Related Tools

Related Posts

What Else Do We Do?

FleetPro has a unique suite of free online tools to help you find the right car.

Take a look at some of our amazing calculators and decision tools for new car buyers.

-

Lease or Buy?

Could you lease a new car for less than the cost of buying? Our lease calculator will work out the best finance method for you. -

ICE or Electric?

Would an electric car be cheaper than petrol or diesel? Our ICE or electric calculator compares running costs instantly. -

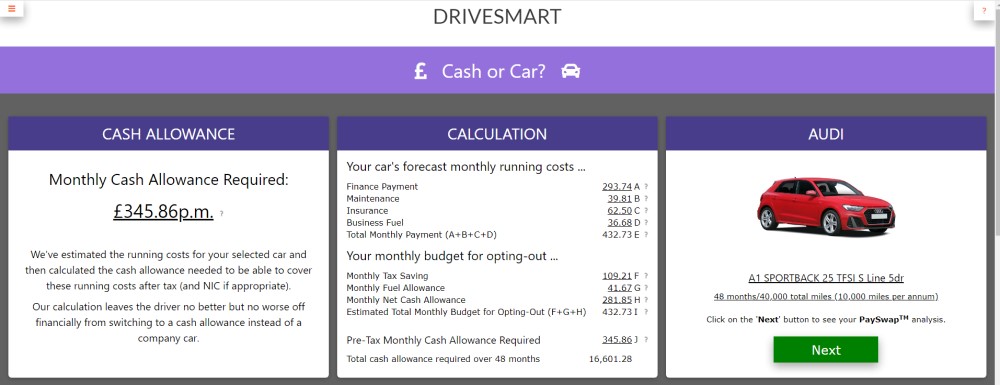

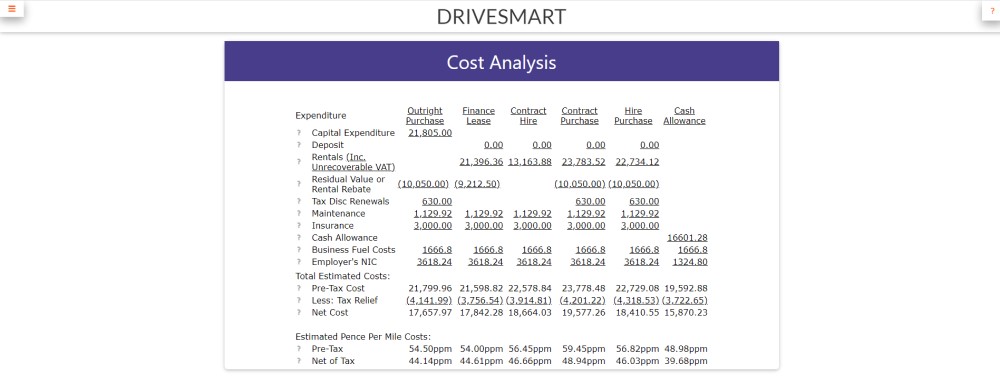

Cash or Car?

Could you give up your company car for a cash allowance? Our 'cash or car' calculator will tell you. -

Car Search

Find your next new car by monthly payment, standard equipment, performance, economy and more .... -

fleetpro.co.uk

Why not visit our fleetpro.co.uk website and see for yourself the amazing range of tools and analysis? We'll keep your place here while you browse.