The FleetPro Blog: What Is Finance Leasing?

We explain how finance leasing works

What Is Finance Leasing?

What Is Finance Leasing?

7 July 2020

It's yours, but it isn't ...

We explain how Finance Leasing works

Finance Leasing is a way of getting to use a vehicle without taking ownership of it.

So basically, the vehicle is yours to use but it's actually someone else's.

You borrow a vehicle over a fixed period (or 'term'), usually a number of months or years during which the vehicle is still owned by the leasing company (the 'lessor') but is rented to you (the 'lessee') for a monthly fee.

What Do You Pay For?

During the lease term you pay a monthly rental to cover costs incurred by the leasing company to operate the vehicle, plus a profit too.

Basically you pay for:

- The cost of the vehicle

- Interest on the money borrowed by the leasing company to buy the vehicle

- The leasing company's profit margin (which might be just the interest charges)

- Sometimes the Vehicle Excise Duty - otherwise known as the 'tax disc' is included too

Depending on the exact terms of the lease, sometimes at the end of the lease you return the vehicle to the leasing company which then sells it and shares the proceeds with you (known as a 'rental rebate').

Other times the monthly rental is lower and you just pay for depreciation and finance. Then, at the end of the lease term, you pay a final instalment (a balloon payment) and you can continue leasing the vehicle for as long as you need, subject to a small administration fee each year (a 'run-on' clause).

There are other permutations of these arrangements too, but the principle is the same - a leasing company finances the vehicle and you pay to use it.

Advantages of Leasing

Because the leasing company recovers VAT on the purchase price of the vehicle the monthly rentals are lower than comparable finance instalments for Contract Purchase, though VAT is then added to the monthly payment.

Because the vehicle is leased, the normal responsibilities of ownership, such as sourcing the best deal and obtaining the best resale (or 'residual') value, are avoided, as is the risk of the residual value being less than expected.

In effect, you simply operate the vehicle rather than owning it.

Disadvantages of Leasing

If the lease agreement is terminated earlier than expected then you may be required to pay an early termination penalty (usually a number of months' rentals).

In addition, if a balloon lease is used then a fixed mileage is normally agreed for the term, so if the vehicle is returned with more mileage than that agreed, or is not in a condition appropriate for it's age and the lease mileage, then 'end of contract' charges may be made by the leasing company.

Should You Lease Or Buy?

Leasing also carries with it the same restrictions as contract hire regarding recovery of VAT on the lease rentals and tax relief for cars with higher CO2 outputs, so you need to be aware of these.

You can see the cost of leasing a vehicle compared to buying it using our lease comparison tool.

Related Tools

Related Posts

What Else Do We Do?

FleetPro has a unique suite of free online tools to help you find the right car.

Take a look at some of our amazing calculators and decision tools for new car buyers.

-

Lease or Buy?

Could you lease a new car for less than the cost of buying? Our lease calculator will work out the best finance method for you. -

ICE or Electric?

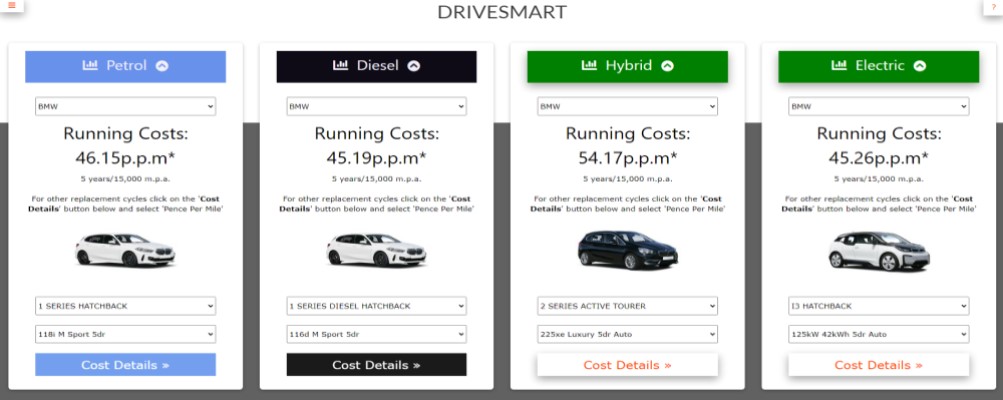

Would an electric car be cheaper than petrol or diesel? Our ICE or electric calculator compares running costs instantly. -

Cash or Car?

Could you give up your company car for a cash allowance? Our 'cash or car' calculator will tell you. -

Car Search

Find your next new car by monthly payment, standard equipment, performance, economy and more .... -

drivesmart.co.uk

Why not visit our drivesmart.co.uk website and see for yourself the amazing range of tools and analysis? We'll keep your place here while you browse.